In the world of accounting and financial statement preparation according to International Financial Statement Standards ( IFRS ), there are certain types of assets and transactions for which it is not easy to find a “market price” to reference. This requires financial models and the expertise of a third party, or an independent financial advisor.

Regarding the two issues… ” It happens frequently, but it’s difficult to assess accurately.” The problem that causes the most headaches for both accountants and auditors is undoubtedly:

1.Valuation of share purchase rights or shares granted to employees ( Share-based Payment – IFRS 2)

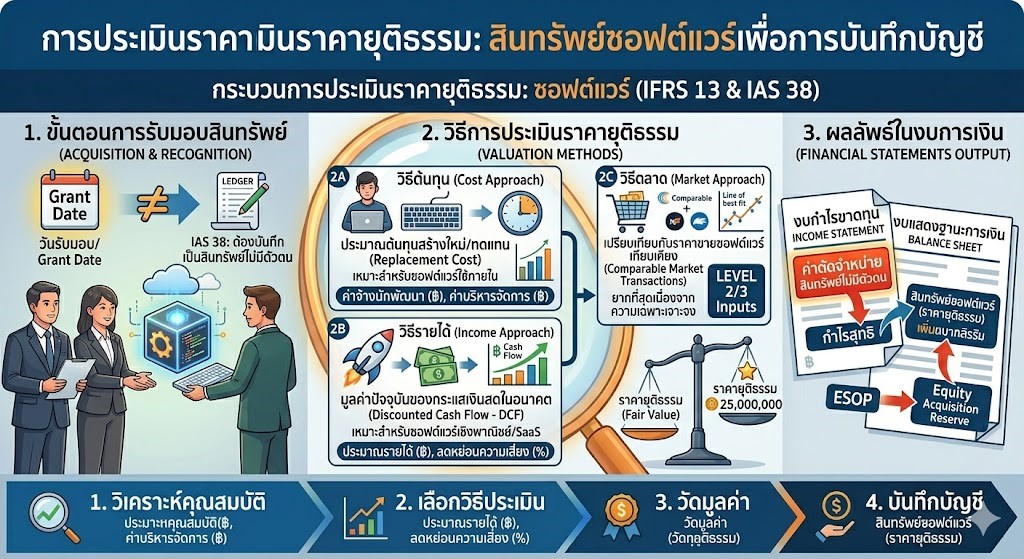

2. Valuation of intangible assets: software/platforms ( Software & Technology Valuation – IFRS13 & IAS 38)

- Share-based Payment (IFRS 2) — When “shares” or ” options” become expenses.

Many companies use the strategy of giving stock or stock options ( ESOP) to executives or employees as a form of incentive, but under certain standards… IFRS 2 (Share-based Payment) These have economic value, and companies must record them. ” Employee expenses” In the income statement as of the grant date. - Software & Technology Valuation (IFRS13 & IAS 38) — Providing a tangible valuation for digital assets.

In the era of Digital Transformation, many businesses develop their own software, platforms, or applications internally ( Internally Generated Software) or acquire them through mergers and acquisitions ( Business Combination – IFRS 3). According to the standard… IAS 38 (Intangible Assets) This software can be converted into an asset on the balance sheet if it proves to have economic value and generate future revenue.

Compare the challenges and solutions in valuation.

| Types of assessment | Relevant accounting standards | The main challenges we will face. | Methods and models used |

| Share-based Payment (Stock –ESOP / Option) | IFRS 2 | • Calculating the volatility of unlisted stocks .

• Conditions for receiving benefits |

It depends on the case, but Discounted Cashflow should be used to understand the benefits that are equivalent to receiving them in monetary terms.

|

| Software / Platform | IFRS13 / IAS 38 | • Software technology changes rapidly.

• Proving the source of income and economic benefits. |

It depends on the case, but Discounted Cashflow should be used to understand the benefits arising from its use. |

Why choose an “independent appraiser”?

For highly complex items such as… IFRS 2 and IAS 38 In-house calculations often face intense pressure and scrutiny from auditors.

- Credibility from the Auditor’s Perspective: A valuation report from an independent, professionally neutral appraiser will help reduce disputes regarding the assumptions used in the calculations.

- Techniques and models that meet international standards: We have updated and internationally reliable financial models and industry databases to support every piece of evidence.

- Save time and reduce the risk of delayed financial statements: Accurate calculations and preparation of supporting documents for assessments from the outset help to speed up and smooth the financial statement closing and audit process.

Eliminate the worry of closing financial statements. Work with professional valuation experts.

at Ira Advisory Company Limited We are advisors and experts in fair value valuation of intangible assets and stock-based payments in accordance with TFRS/IFRS standards , with experience and models accepted by leading auditors.

- Services for calculating and valuing Share-based Payments (IFRS 2).

- Software, platform, and technology valuation services ( IFRS 13 & IAS 38).

Enhance the credibility of your financial statements and ensure a smooth audit process with our services.

Contact us today to schedule a consultation and plan a property valuation with our experts.